Reconciliation must be performed on a regular and continuous basis on all balance sheet accounts as a way of ensuring the integrity of financial records. The company should ensure that any money coming into the company is recorded in both the cash register and bank statement. If there are receipts recorded in the internal register and missing in the bank statement, add the transactions how much of my internet expenses are deductible on my 1040 to the bank statement. Consequently, any transactions recorded in the bank statement and missing in the cash register should be added to the register. It verifies the accuracy of account balances by comparing a company’s internal records with those in its external accounting system.

In this article, you will learn everything you need to know about account reconciliation including how account reconciliation software works. Parent companies use this to bring together all the accounts and ledgers from the subsidiaries they may have. The process looks for mismatches both within and between any of the subsidiaries. It provides an opportunity to record their cash position and forecast their cash flow with a higher degree of accuracy.

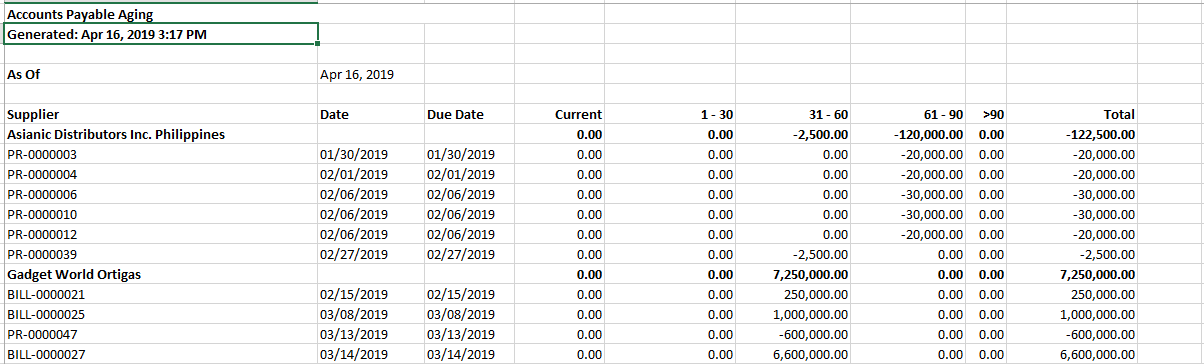

What is the Account Reconciliation Process?

- Sage Intacct integrates with CRM, HR, and eCommerce platforms, making it easier for businesses to manage their finances across different departments.

- With OneStream XF’s account reconciliation module, users can easily manage large volumes of transactions.

- In this case, businesses estimate the amount that should be in the accounts based on previous account activity levels.

- Account reconciliation should be prepared and carried out by qualified accounting personnel, typically within the finance department.

Understanding the different types is crucial for maintaining financial accuracy and transparency. Whether it’s reconciling bank statements, vendor accounts, or intercompany transactions, each type plays a pivotal role in ensuring that records are consistent and errors are promptly identified and corrected. The reconciliation process involves comparing internal financial records with external documents to identify and correct discrepancies.

Account reconciliation is an accounting process, usually embarked on at the end of an accounting period, that makes sure financial accounting records are consistent and accurate. Generally done for general ledgers, account reconciliation involves the comparison of two independent but related records to make sure that transactions and balances correspond with each other. The purpose of reconciliation is to ensure the accuracy and ethics of a business’s financial records by comparing internal accounting records with external sources, such as bank records.

Access Exclusive Templates

Additionally, account reconciliation software can provide real-time insights into cash flow, enabling business owners to make better-informed financial decisions. Oracle NetSuite is a cloud-based accounting software that offers accounts reconciliation, invoicing, and other financial management features. For example, real estate investment company ABC purchases approximately five buildings per fiscal year based on previous activity levels. This year, the estimated amount of the expected account balance accounting for inventory write downs is off by a significant amount. The documentation review process compares the amount of each transaction with the amount shown as incoming or outgoing in the corresponding account. For example, suppose a responsible individual retains all of their credit card receipts but notices several new charges on the credit card bill that they do not recognize.

For instance, when you receive a check from a customer, you may have recorded it as paid. But there are chances that the check could have bounced due to numerous reasons. A three-way reconciliation is a specific accounting process used by law firms to check that the firm’s internal trust ledgers line up with individual client trust ledgers and trust bank statements. For lawyers, this process helps to ensure accuracy, consistency, transparency, and compliance.

The process of reconciliation confirms that the amount leaving the account is spent properly and that the two are balanced at the end of the accounting period. The software allows users to easily reconcile accounts from multiple sources, including bank accounts and credit cards. And generating financial reports in Clio Accounting is a breeze, making your life, and your accountant’s life that much easier. The goal of bank reconciliation is to check that ending balances match on both your bank statement and your records. Should there be any discrepancies that come up through the reconciliation process, you can then take action to resolve them.

Reconciliation in accounting best practices

Clio’s legal trust management software, and Clio Accounting both provide lawyers with the ability to conduct trust account reconciliation–helping to keep your firm compliant and your client’s funds secure. In order for reconciliation in account to be most effective in preventing errors and fraud, it’s important to conduct the process frequently. And, for some types of accounts, like trust accounts, there may be specific frequency requirements that you must follow to stay compliant with your state bar. All trust transactions what is the main focus of managerial accounting in the internal ledger should be accurately recorded and should align with transactions in the individual client ledgers. Some businesses with a high volume or those that work in industries where the risk of fraud is high may reconcile their bank statements more often (sometimes even daily).

Account reconciliation processes ensure the total sum leaving an account (or accounts) matches the amount spent. Once you have access to all the necessary records, you need to reconcile, or compare, the internal trust account’s ledger to individual client ledgers. Reconciling the accounts is a particularly important activity for businesses and individuals because it is an opportunity to check for fraudulent activity and to prevent financial statement errors. Reconciliation is typically done at regular intervals, such as monthly or quarterly, as part of normal accounting procedures. Individuals should reconcile bank and credit card statements frequently to check for erroneous or fraudulent transactions. After 60 days, the Federal Trade Commission (FTC) notes, they will be liable for “All the money taken from your ATM/debit card account, and possibly more—for example, money in accounts linked to your debit account.”